Adjusting Financial Statements: A Complete Guide

The normalization of your financial statements involves making numerous adjustments to calculate SDE or EBITDA.

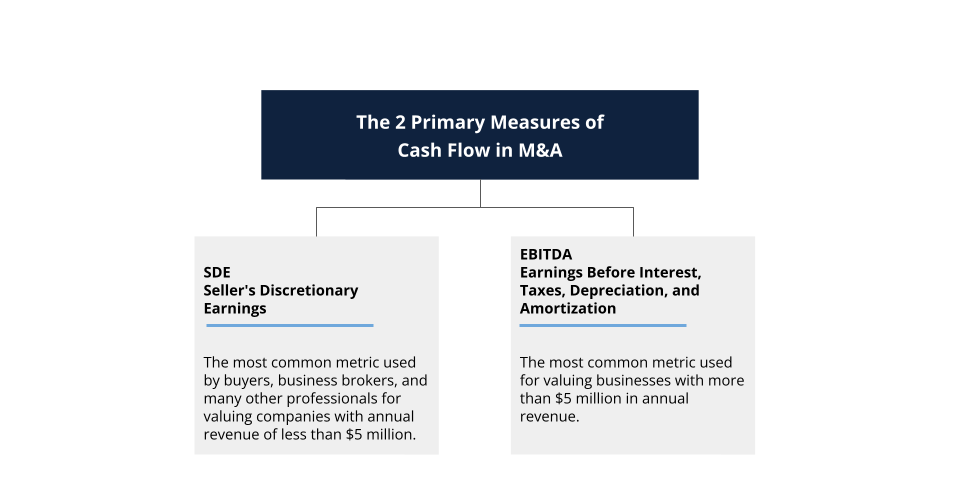

- SDE is the most common metric used by buyers, business brokers, and many other professionals for valuing companies with annual revenue of less than $5 million.

- EBITDA is the most common metric used for valuing businesses with more than $5 million in annual revenue.

Common adjustments to financial statements:

- All owner’s salaries and perks

- Family members’ salaries and perks

- Expenses or income that aren’t expected to recur or continue after the sale

- Personal expenses not related to the business, such as personal auto, insurance, cell phone, child care, medical, and travel expenses

- Depreciation

- Amortization

- Interest payments on any business loans

- Investment or other non-operating expenses or income

- Other one-time or non-recurring expenses

- Non-operating revenue

Tips for Making Adjustments

- Be Thorough: All adjustments should be concise, verifiable, thorough, and accurate. The more detail you provide to the buyer, and the more you back up your reasoning for adjustments with documentation, the more likely your business will sell quickly and for the best possible price.

- Be Conservative: When selling a business, always be conservative when making adjustments to your financials. The fewer adjustments, the cleaner your financials will look. Eliminate any adjustments less than 0.5% to 1.0% of your SDE or EBITDA, and ideally, all adjustments before selling your business.

How To Produce a Detailed List of Adjustments

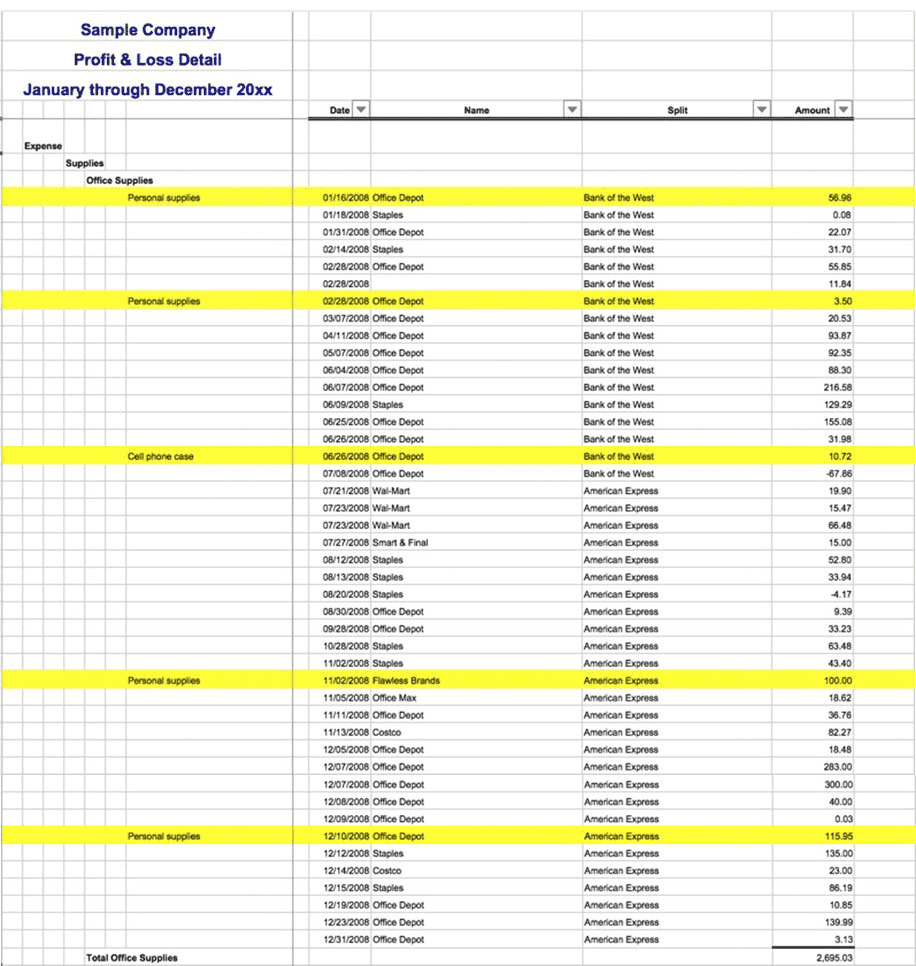

- The best way to prepare a list of your adjustments is to export a “General Ledger” (called a Profit and Loss Detail report in QuickBooks) from your accounting software to a spreadsheet, such as Microsoft Excel or a similar program. Once you’ve exported this to a spreadsheet, simply mark each adjustment with an “X” or highlight the entire row.

Introduction

Like most business owners, you probably operate in a way that keeps your taxes low.

You may have given yourself and your family members perks and benefits, kept offspring on the payroll, and written off other expenses through your business – all of which contribute to decreased earnings and lower taxes.

All well and good. But when the time comes to properly value your business, your financial statements must be “normalized” or “adjusted” to form the basis of an accurate evaluation.

This involves numerous calculations to arrive at the true earning capacity of your business and is one of the most important steps in preparing your business for sale.

How Your Financials Are Adjusted in M&A

Making adjustments to your financial statements involves removing owner-specific perks, benefits, and expenses. This process is necessary to show potential buyers your business’s available cash flow.

Adjusting the financials allows you to compare your business with other businesses using seller’s discretionary earnings (SDE) or earnings before interest, tax, depreciation, and amortization (EBITDA).

- SDE is the most common metric used by buyers, business brokers, and other professionals for valuing companies with annual revenue of less than $5 million.

- EBITDA is the most common metric used for valuing businesses with more than $5 million in annual revenue.

Buyers compare potential acquisitions using SDE or EBITDA. By comparing the SDE or EBITDA of one company with another, buyers can easily understand a business’s value based on its actual profit rather than its taxable income. This provides a more accurate comparison between target companies.

Definitions of Adjustments

The following are descriptions of the different types of adjustments:

Conclusion

Trading efficiently in the eyes of the taxman and in the eyes of your potential acquirer can be two entirely different things.

Closing that gap fairly and demonstrably is a key phase in properly valuing your business and preparing it for sale. But the process of normalization isn’t simple – you must pay careful attention to the lists above to determine which benefits can be adjusted and which can’t.

In life, as in business: proceed with cautious optimism and act early. Neutralize potential discrepancies before they arise, and you’ll be another step closer to the right sale price for your business.